As an angel investor, I’m not buying into the SaaS sell-off as proof that software is dead. What’s happening is something more specific and more useful to understand. Public markets are repricing software based on what’s defensible in an AI-native world.

Many moons ago, I completed my degree in economics. I’ve always been drawn to data. So when I started seeing headlines about a “tech collapse,” I couldn’t reconcile the narrative with what I knew: many of these software companies were still growing their customer base, expanding revenue, and actively innovating across their portfolios.

Since this piece is about the impact of AI, my thesis was that the selloff was more nuanced and I decided to use AI to explore the issue. Using Claude Cowork to analyse share price trends for listed SaaS companies over the past 12 months – what’s telling is that this would have taken my old team at PwC days to complete. This time it took me alone about two hours to complete with a bit of fine-tuning. 1. Although there was an annoying two hour delay when I ran out of claude credits.

Think of it like the Sorting Hat at Hogwarts: the market isn’t banishing software altogether; it’s deciding where each company truly belongs. That distinction matters.

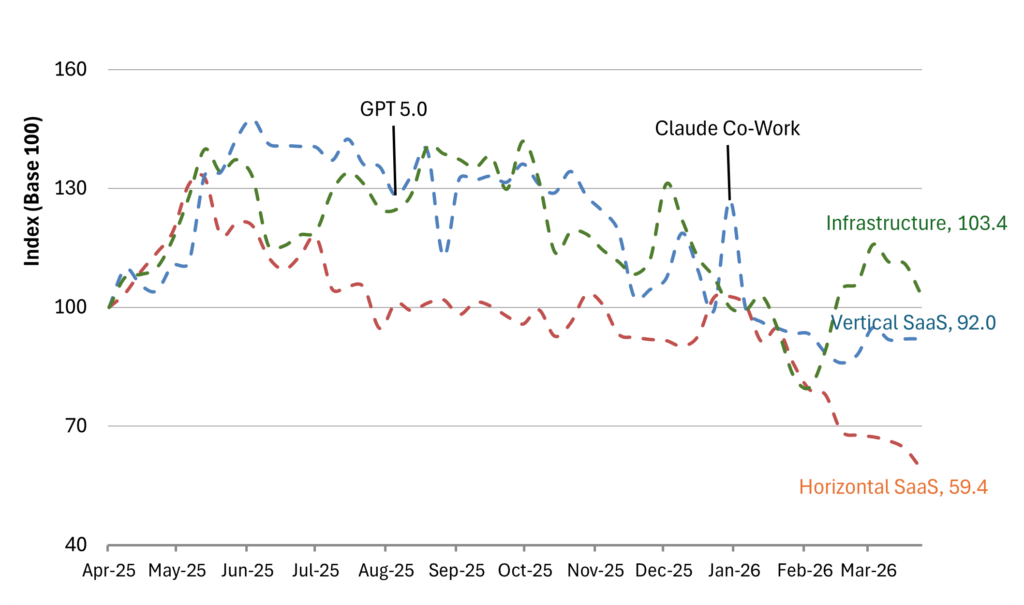

As can be seen in the graph, it isn’t a uniform collapse; it’s the market starting to separate businesses AI can strengthen from those it can increasingly absorb. Over the past 12 months, horizontal SaaS has taken the hardest hit. Vertical SaaS is down, but far less so, and infrastructure has largely stayed protected.

And that sorting mechanism is exactly where the opportunity lies for early-stage investors paying attention. Knowing which “house” your startups belong to makes all the difference. The gap is the signal – the market’s distinguishing companies AI can amplify from those it can replace.

Three broad categories that matter

Vertical SaaS is software built for a specific industry or tightly defined workflow. Its data models, compliance logic, and operational processes are native to that domain, which makes it hard to generalise and harder to replace.

Horizontal SaaS cuts across industries. It supports common business functions like CRM, HR, finance, collaboration, and task management, where the same product can serve many sectors with relatively little adaptation.

Infrastructure sits deeper in the stack. It includes cloud platforms, APIs, developer tools, data pipelines, identity, and security systems that enable other software to be built, deployed, and operated.

| Horizontal SaaS | Vertical SaaS | Infrastructure | |

| Companies (n) | 54 | 52 | 27 |

| Median Return | 59% | 92% | 103% |

| Mean Return | 71% | 83% | 112% |

| % Positive | 11% | 23% | 41% |

| Best | 214% | 308% | 215% |

| Worst | 12% | 25% | 27% |

The pressure on horizontal SaaS is the easiest to understand. Many horizontal products were built around generic workflows like coordination, summarisation, communication, and routing. Those are exactly the layers AI is getting better at absorbing. In some cases, AI is not just improving the product. It is making the product itself less necessary.

The market data reflects that pressure. Only 11% of horizontal SaaS companies in the sample were in positive territory over the period, compared with 23% for vertical SaaS and 41% for infrastructure.

There is also a nuance that matters here – some of the most interesting opportunities may sit beneath traditional infrastructure categories, especially in data layers tied to emerging compliance regimes. Over time, every organisation may need a trusted and auditable source of truth. In that world, the winner will not be the best dashboard. It will be the best foundation.

Xero is a useful example of the broader point. It is not vertical SaaS. It is horizontal accounting software. But once it becomes the financial system of record, the relationship changes. At the start, a company is simply a customer. Over time, with years of transaction history, integrations, reporting logic, reconciliations, and tax workflows embedded in the system, that customer starts to look much closer to a captive.

Xero recently inked a deal with Anthropic to embed AI into its popular accounting platform. Xero is attempting to show investors the benefit from the increasing uptake of artificial intelligence rather than see its subscription business model eroded by it 2.

That is why the public market message needs more precision than a generic software sell-off narrative allows. Shallow horizontal tools are exposed. Deeply embedded systems of record are much more defensible. Both may be sold down in a risk-off cycle, but the shallow ones are being punished much harder.

Implications for an angel investor

That distinction has direct implications for what I do as an angel investor. Opportunities in AI infrastructure and vertical AI still look attractive because those are categories where defensibility can be built and compounded over time. Horizontal AI looks far less compelling unless there is a very clear moat in proprietary data, workflow ownership, regulatory complexity, or control of a mission-critical system of record.

Two recent investments we have made illustrate the kind of opportunity that fits this view. Avarni is building emissions data infrastructure as carbon disclosure moves from voluntary to mandatory under frameworks such as CSRD, ISSB, and SEC climate rules. Its value lies in ingesting messy supplier data, normalising it against recognised frameworks, and becoming the trusted foundation for reporting and auditability. The more suppliers that are onboarded and the more audit trails that accumulate, the harder the platform becomes to replace.

Tendl sits in a different category but follows the same logic. Tender response is a high-friction, document-heavy workflow where context, accuracy, compliance, and execution all matter. This is where AI becomes strategically interesting, not as a novelty layer, but as a way to improve performance inside a workflow that is already mission critical. What makes that defensible is not just the model. It is the accumulation of workflow-specific context over time, including prior bids, pricing logic, compliance requirements, and the language that actually wins in a given sector. Every tender strengthens the underlying data asset. That is a very different dynamic from a horizontal AI writing tool with little memory, low switching costs, and weak customer captivity.

Conclusion

The more constructive read on this moment is that the sell-off isn’t just destruction, it’s a sorting mechanism. It’s forcing founders and investors alike to ask tougher questions about product depth, workflow ownership, customer dependence, proprietary data, and whether the software being built will still matter as AI keeps improving.

The real lesson from public markets is not that SaaS is over; it’s that generic software is increasingly vulnerable in the age of AI. For early-stage investors, that means focusing on where the real moat sits (in proprietary data, workflow ownership, switching costs, or system-of-record status) and on whether a product merely attracts customers because it’s novel or keeps them because it becomes indispensable.

If this is of interest – reach out anytime. At MooCoo Ventures, we spend our time identifying and backing early-stage companies that are building the next generation of defensible software, startups with genuine workflow depth, high switching costs, and durable data advantages in an AI-driven world.

If you’re in Brisbane, Brisbane Angels is a great local starting point. If you’re outside South East Queensland or want a more digital experience, the MooCoo syndicate lets you invest in curated early-stage deals through our digital platform.

Equally, if you know founders or investors thinking about their next chapter, we’d welcome introductions to anyone keen to explore the kind of opportunities this market moment is revealing.

References

- Source Data: yfinance (open source financial data from Yahoo Finance). Analysis includes listed SaaS companies on U.S. and international exchanges, categorised as vertical SaaS, horizontal SaaS, and infrastructure based on MooCoo Ventures categorisation. Market data as of 27th March 2026. ↩︎

- https://www.afr.com/technology/xero-inks-anthropic-deal-insisting-ai-can-help-software-giants-20260324-p5ujl0 ↩︎