Something subtle has shifted inside MooCoo Ventures over the past year or two. AI hasn’t arrived with fanfare, and it hasn’t replaced anyone outright. It has just… settled in. Quietly. Gradually. And now it sits inside the machinery of how we get things done.

It reviews pitch decks, speeds up research, interrogates investment theses, supports due diligence, and pulls everything together into structured deal reviews. Work that once took analysts days, is increasingly managed by something closer to an always-on assistant.

The gains are obvious. The process is faster, more organised, and able to cover more ground with a smaller team. But as these systems have become more capable, they’ve also made something clear that was easy to miss when analysis itself was scarce.

The real work in angel investing was never just the analysis, but the judgment applied to it.

The compression of the analyst layer

That’s why the current debate about whether AI will replace investment teams feels slightly off. It’s not quite the right question. What’s actually happening is narrower, but more important. AI is compressing the analysis layer. The manual work of gathering, synthesising, and structuring information is being reduced to something close to instant. That doesn’t remove the need for investors, but it does shift where their value sits.

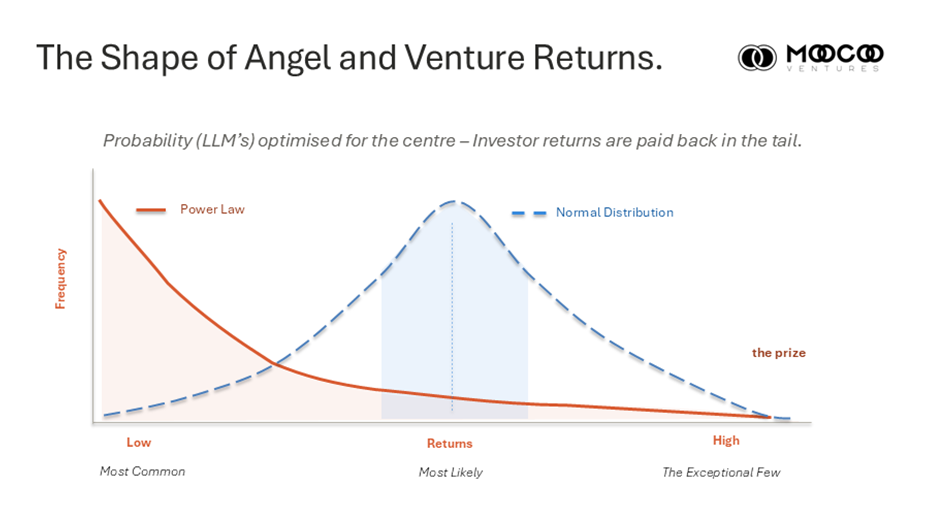

To see why, it helps to be clear about what these systems are. Large language models are not rule-based engines; they are probabilistic machines. They generate outputs by estimating what is most likely to come next. For all the ways we talk about them, they aren’t built to identify what is exceptional. They’re built to converge on what is typical.

The problem with the centre

In practice, that makes LLMs extremely good at summarising the familiar and organising the mainstream view. But venture and angel investing doesn’t operate in the middle of the distribution. It operates in the tail. Returns follow a power law, where a small number of investments account for the vast majority of outcomes. Most companies sit somewhere around the middle. That’s just not where most of the value is created.

This creates a quiet tension. A probabilistic system will tend to pull analysis toward the centre, because that’s where confidence is highest. The investor, by contrast, has to recognise that the centre is the wrong place to look.

The most valuable opportunities rarely look obvious at first. They tend to show up as something slightly off – a founder who doesn’t fit the usual pattern, a market that seems too small, or an idea that feels awkward before it feels inevitable.

When more information raises the bar

As AI takes over more of the analytical work, this distinction becomes sharper, not less relevant. Having more structured information doesn’t reduce the importance of judgment. If anything, it raises the bar. The bottleneck is no longer producing analysis. It’s interpreting it well. Knowing what matters, what can be ignored, and when something that looks like an outlier might actually be the point.

The risk of convergence

There’s also a second‑order effect worth paying attention to. As more investors rely on similar models (trained on broadly similar data) there’s a risk that early‑stage investing becomes not just faster, but more uniform. If everyone is drawing from the same synthesis and arriving at similar conclusions, then the advantage of better information starts to fade. The edge moves elsewhere. In that kind of environment, differentiation depends less on access and more on the courage to think differently. The real advantage comes from my willingness to step deliberately away from what the model suggests, and to trust my experience and context when the consensus is not yet aligned.

AI provides the investment realism. Only you can provide the optimism

Ultimately, this is where judgment becomes the truly scarce asset. It is not because AI is weak, but because it is strong in ways that are becoming widely available. The more effectively these systems guide me toward the centre, the more valuable it becomes for me to recognise why the centre is exactly where I shouldn’t be standing.

To navigate this, I lean on a dual framework: irrational optimism and uncompromising realism.

I need irrational optimism to lean into the improbable. Without that, I would just be a sceptic, caught in a cycle of overthinking, over-analysing, and delay. It is the optimism that allows me to back the founder or the market that doesn’t yet make sense on paper. But that must be balanced by uncompromising realism. When the facts change, I must be ready to change my mind immediately. I have to act on what is actually happening, not what I want to be true.

This is where AI acts as the perfect foil to human intuition. I use AI for the uncompromising realism, to strip away the narrative, pressure-test the data, and force me to look at the cold facts. But I reserve the irrational optimism for myself. AI can tell me the probabilities, but it cannot decide when to bet against them.

I find that Ai is sharpening my process, making it faster, more systematic, and far better informed. But it cannot solve the core conundrum of early stage investing: the leap of faith required to back something that looks improbable.

On this, I’m unashamedly old school. Data can confirm a trend, but it cannot manufacture conviction. I find it impossible to imagine a time when I’d delegate that final, human choice to a soulless agent. Because in the end, it is my own irrational optimism that writes the check, and my own uncompromising realism that accepts the risk.